Occupiers have joined anti-foreclosure advocates to occupy home auctions and abandoned buildings and block foreclosures. A few state attorneys general have begun resisting the Obama administration’s awful mortgage fraud settlement and started investigating banks and servicers. Even shareholders are in revolt, filing class action suits against their companies. By one measure, student loans are one of the biggest concerns amongst supporters of Occupy Wall Street. There is now an OccupyStudentDebt. A petition to forgive student loans has gathered 300,000 signatures and was included as part of a general debt forgiveness bill on the floor of the House of Representatives. Congress has even begun to touch on medical debt issues.

Taken together, we can say that these and other actions are the sign of growing resistance to key aspects of the social model of the past 30 to 40 years. We have been living in a society where debts, rather than rights, have been the major means for accessing basic social goods like housing, education, and health care. That social model was built around the assumption that while real incomes stagnated and the state did not directly provide many basic goods through universal entitlements, cheap credit would do the trick instead. High finance was inextricably intertwined with the privileges of citizenship. This was not a very good social model. With any luck, and a serious amount of political action, current resistance could lead to alternative ways of thinking about how we make these goods available to all.

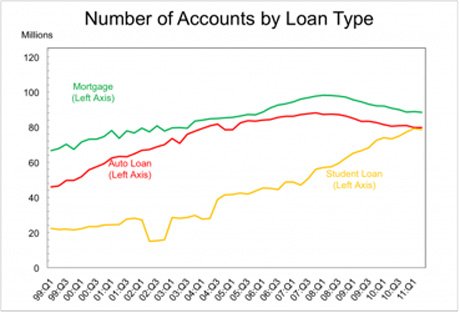

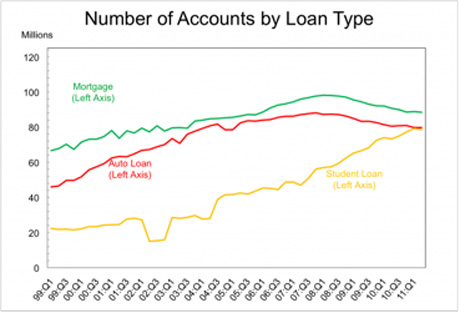

After all, while the previous decade has been represented as a debt-financed spending binge when consumers lived well beyond their means, it turns a complex story into a morality play. A major part of the credit ‘binge’ was about necessities, not luxuries. Sub-prime mortgages (especially with the decline of affordable housing) were the only way for many to become homeowners. Similarly, student loans were the only way for many to gain access to higher education and thus participate as equals in the radically unequal distribution of opportunity in the United States. The total value of student loans has surpassed total credit card debt, and is projected to top $1 trillion later this year. Mike Konczal posted the following graph at Rortybomb showing the dramatic rise of student debt. In a decade, student loans have gone from a third of consumer loans to far more than half.

We find a similar story in health care. Two major national studies of medical indebtedness by a group of scholars, including Elizabeth Warren, have shown that illness and medical costs are a major cause of household bankruptcy. They noted that by 2001 “illness or medical bills contributed to about half of bankruptcies.” Notably, in their 2001 study, they found that 75.7 percent of medical debtors had insurance at the onset of illness. Underinsurance, as much as lack of insurance, was a major financial burden. So too was loss of income due to illness (by their estimate, income loss is 40 percent of medical-related indebtedness). Worse yet, their follow up 2007 study of medical indebtedness notes that the “number of un- and underinsured Americans has grown; health costs have increased; and Congress tightened the bankruptcy laws.” That has led to a 50 percent increase in the proportion of bankruptcies attributable to medical problems. These bankruptcies, moreover, occurred in families only marginally worse than the median income and occupational class of American citizens. Once again, indebtedness is the product of the 99% trying to meet the costs of a basic good — health care.

If there is a reasonable expectation that debtors can meet their interest payments then in theory debt is not a particularly bad way to finance access to certain goods. It is on the individual borrower to make a judgment about what constitutes a reasonable debt burden.

There are, however, two problems with this theoretical view. First, there might be very good social reasons to not want to yoke access to certain social goods to debt. Education is a prime example. Taking on debt means accepting a kind of discipline. One must make all future calculations about, say, educational and career choices with the need to meet future interest payments in mind. In conscious and unconscious ways this narrows horizons and produces a more instrumental relationship to education. In college I saw concerns about debt shape decisions about which classes to take and what to major in. I also saw many of my college classmates make more conservative professional choices (corporate law, consulting, finance, medical specialist) than they might otherwise have made (public service, teaching, science, public interest law) in order to ensure their ability to pay back loans. This appears to have been a pattern. A study of educational and career choices in the early 2000s by Princeton economists has found that “debt causes graduates to choose substantially higher-salary jobs and reduces the probability that students choose low-paid ‘public interest’ jobs.”

It is frequently observed that the growth of finance sucked up the math and physics geniuses, who might have contributed something lasting to society, into hedge funds and investment banks to ruinous effect. But the alteration of professional choices is much wider than that. The number crunchers at the top were, one suspects, lured away by lucrative pay. The much more widespread, and difficult to measure, shift in career choices due to the discipline of debt burdens is probably the more important, and still ongoing, consequence of high student loans.

If access to higher education were on the order of something like a right — a publicly financed good, provided at little or no cost, to ensure real equality of opportunity — then one can imagine a much different set of results. While conservatives like to talk about ‘freedom,’ this is a place where the left ought to have the upper hand in connecting economic practices to real freedoms. Providing necessary social goods, especially education, as a right rather than through debt not only reduces the disciplining effects of the latter. It also is a way of publicly recognizing and democratically defending the real freedoms of all citizens.

To be clear, this is not a moralistic criticism of debt as evil or irresponsible. But there are very good reasons why society would not want to impose certain kinds of discipline on (most of) its citizens. Firstly, from a social point of view, people’s talents might be much more productively used in some other area than those that promise the most immediate monetary returns. There is no shortage of aspiring bankers and traders, but there is a primary care doctor shortage. Primary care doctors can graduate medical school with as much as $200,000 in debt.

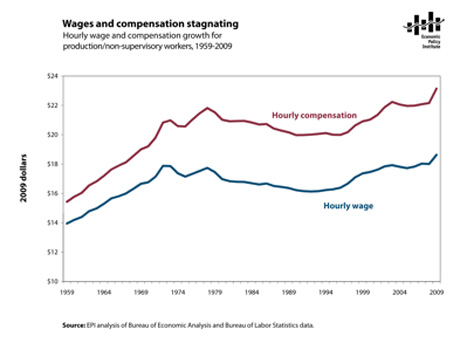

A second reason is that practice does not resemble theory. Again, the theory is that so long as each individual makes a reasonable calculation about his or her ability to meet debt payments, there is nothing wrong with financing access to basic social goods through credit. Putting systematic fraud aside (but remembering it is unlikely that credit can sink that far into housing and educational markets without it), there is a deep historical reason for thinking that practice was the opposite of theory. The rise of debt-financed household consumption generally was the product of stagnating wages. Consider, for instance, this research by the Federal Reserve Bank of San Francisco comparing the growth of debt, wealth, and income:

Or compare the above growth of household debt with the stagnation of wages and benefits during that same period (from State of Working America):

Debt-financed consumption was, in other words, a response to the declining ability of most households to afford existing rates of consumption, not an increasing ability or trust in future ability to pay back that debt.

The entire social model, then, was built on a lie. The separation of consumption (financed by future promises to pay) from production (based on limiting present ability to earn) was a mirage. The problem has been that the underlying right to maintain a certain standard of living, or even to access to certain basic social goods like housing, health, and education, was just that: implicit. Every so often, of course, it was made somewhat public — for instance when Clinton or Bush would say something about providing housing to the poor and minorities who could not otherwise afford it (mainly by changing market incentives and promoting sub-prime borrowing, as it turned out). But this promise was always implicit and had to stay that way because it was mediated through the credit system. Access to these basic social goods was never a fully public claim each individual had against society. Instead, access to these social goods was a matter of a complex series of private, individualized claims against other private institutions like banks and employers, with the public role submerged in the form of altered market incentives. That is the difference between debt and right, and it is clear that the debt-based social model has failed.

There are certainly some situations where debt-financed consumption is a perfectly good option. For instance, the current call for more fiscal austerity at the federal level is ideological claptrap. Moreover, any economy always has to take a bet on the future if it is going to innovate, especially since innovation always comes with the risk of failure. But there are certain kinds of basic goods that are better provided as a matter of universal right, both for the sake of the freedom of the persons who need those goods and as a matter of economic efficiency and productivity. We can have risk-averse graduates and a chronically ill workforce chained to underwater mortgages, or we can have healthy, well-educated citizens with enough security, and thus freedom, to take real risks in their lives.

Join us in defending the truth before it’s too late

The future of independent journalism is uncertain, and the consequences of losing it are too grave to ignore. To ensure Truthout remains safe, strong, and free, we need to raise $47,000 in the next 8 days. Every dollar raised goes directly toward the costs of producing news you can trust.

Please give what you can — because by supporting us with a tax-deductible donation, you’re not just preserving a source of news, you’re helping to safeguard what’s left of our democracy.