Here comes another billionaire who thinks that anyone who talks about income inequality is a Nazi; this time it’s Ken Langone, the co-founder of Home Depot. I don’t have anything useful to say about this, other than observing that there must be a lot of these guys.

I mean, there aren’t that many billionaires. Our sightings of multiple examples of the genus that not only believes that progressives are just like Hitler but will say so in public must indicate that a substantial proportion of our billionaires share this belief, but they’re more private about it.

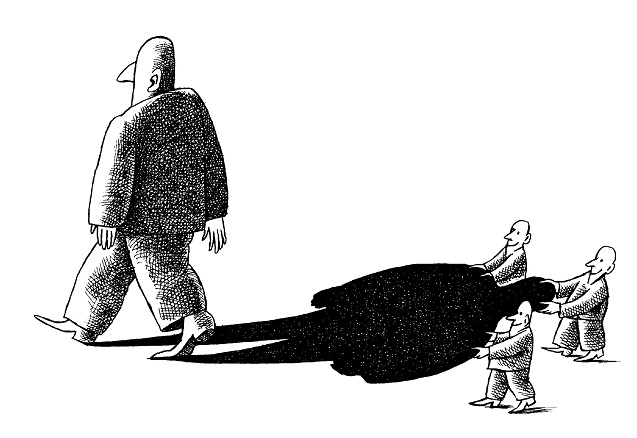

Luckily, great wealth doesn’t bring great political influence in modern America – does it?

Jonathan Cohn’s recent article on Mr. Langone in The New Republic brought to mind an earlier rant by the same guy on Bloomberg TV, in which he denounced yours truly and my “highfalutin thoughts and ideas.” And I think that this rant (and others like it) gives a partial clue to the mystery of the continuing popularity of the Wall Street “macro canon,” despite its total failure in practice.

What, after all, was Mr. Langone raging against?

Well, me, of course. But not, presumably, against “highfalutin” ideas in general: Mr. Langone can’t really be a stupid man, and I’m sure that when it comes to, say, information systems for inventory management, he’s quite willing to accept the idea that some things are technical and require some knowledge.

No, what I think he’s really raging against are two things. First is the idea that understanding economics, as opposed to other issues, might involve some kind of special expertise. This is an all-too-common problem among the wealthy, and maybe especially among self-made men: they think that their personal financial success means that they understand the economic system, and they bristle at the notion that macroeconomics may be more than the sum of individual business strategies.

The other source of his rage – and this, I think, gets at the roots of the right-wing canon – is his fury at the notion that sometimes scarcity doesn’t rule. For many people on the right, it has to be true – just has to be true – that prosperity is limited by the willingness of productive people (that is, people like them) to produce.

The idea that sometimes the problem is instead a lack of demand, that the failure is a system malfunction rather than a lack of sufficient effort, is anathema. Among other things, it suggests that sometimes people succeed or fail for reasons that have nothing to do with their personal talents and virtues or lack thereof, a suggestion that men like Mr. Langone – who believe that their personal success was entirely earned – find deeply offensive.

And so when anyone says that this is a depressed economy in which deficits don’t crowd out private spending, and in which printing money doesn’t mean inflation that expropriates their hard-earned wealth, they don’t listen to the argument, let alone pay attention to the evidence.

They take it as a personal affront, and start yelling about highfalutin nonsense.

Join us in defending the truth before it’s too late

The future of independent journalism is uncertain, and the consequences of losing it are too grave to ignore. To ensure Truthout remains safe, strong, and free, we need to raise $43,000 in the next 6 days. Every dollar raised goes directly toward the costs of producing news you can trust.

Please give what you can — because by supporting us with a tax-deductible donation, you’re not just preserving a source of news, you’re helping to safeguard what’s left of our democracy.